Delivery providers may be reporting a surge in orders as COVID-19 keeps diners at home, but the pandemic is expected to hurt more in the long term, according to a Wells Fargo financial analyst.

In a research note from John Power, a senior analyst at Wells Fargo who covers the food delivery space, the pain point comes from an expected decline in independent restaurants.

According to the Wells Fargo restaurants team, as high as 25 percent of independent restaurants “will shut down entirely because delivery sales will be insufficient to cover fixed costs such as rent, food and salary.” That’s compared to 5 percent of chain restaurants expected to close.

The calculation comes from past wisdom from the Great Recession and the swath of closure announcements during this pandemic. Year-over-year growth of restaurant food sales fell 7 percent growth prior to the Great Recession to a decline of 1 percent in 2009 as food sales are highly correlated with personal income growth. The historic unemployment rate and presumably rocky road ahead will likely mean similar personal income declines.

Without the scale of chains and their access to capital and the typical shift to value in a down economy, independents will be the hardest hit in a similar scenario. That’s especially damning for delivery providers because independent restaurants are key partners for third-party delivery, and third-party delivery is an ideal solution for many independents.

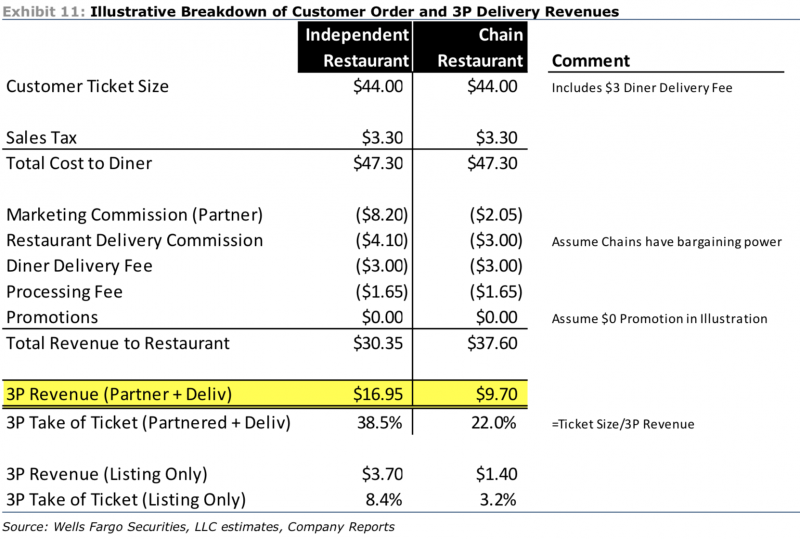

“Chain stores are known to be low-margin customers for the third-party delivery players because many already have sophisticated internal marketing and delivery infrastructure, and most of their business is already through the ‘convenience’ channel, i.e. drive-through, takeaway, and home delivery,” wrote Power. “Because of their low IT and marketing sophistication, independent restaurants and major third-party delivery companies have a strong value proposition for partnership.”

Given that strong value proposition, independents pay more in commissions. Power broke down the revenue from both independent and chain restaurants. As seen below, the take rate for third-party varies drastically between independent and chain restaurants in the estimation of Wells Fargo’s research team. In all, third-party providers see 42 percent less revenue from chains.

Power said that will hurt Grubhub more than Uber Eats or DoorDash because the company has especially targeted non-chain operators. Power added that about 90 percent of Grubhub profits are driven by independent restaurant orders.

That may be showing. Grubhub reported that the key Daily Average Grubs (DAGs) stat is up 10 percent through the first half of April. Uber Eats reported that orders are up 30 percent. The exact cause of that mismatch is unclear, but between full-service independent restaurants closing and Uber’s larger share of chain restaurants where workers typically get lunch could both contribute.

Power didn’t touch on Postmates, but the company is likely seeing similar trends on the dining side as the company also focuses on independent restaurants. But, the company has reported growth in retail sales and convenience-store purchases.

Power maintains an “overweight” (generally a “buy”) rating for Uber and a “neutral” (generally a “hold” rating) for Grubhub, noting that both will be volatile stocks over the next 12 months.